At the end of every year I like to take some time to look back at my last years goals in review and also plan a little bit ahead for the year to come.

Here is the list of goals I set out for myself at the beginning of 2016 and the dates of the ones I completed.

GOALS FOR 2016

Have $150,ooo in my self directed investment account*Complete May 20*

Have $125,000 in my company pension.*Complete July 22*

Get pre-approved for a rental property*Comlete Aug 1st*

Buy a rental property and slum lord it up *NOPE*

Save money for trip to Cuba *Complete June 15*

Earn $6,000 yearly in dividend income*Complete Dec 30*

Have over $30,000 in cash for market crash*Complete June 28*

Open a margin account for market crash (only to be used if Dow drops +40%)*Complete May 3*

I had a very successful year in the market (like everyone else) and finished 7 out of my 8 goals I set for myself.

The single goal I never finished was to buy a rental property. There are several reasons for this but the main one is the house prices here in Vancouver have started to show signs of weakness (YAY!). I don’t want to buy at the top and there is no stop loss on houses.

Some of the goals need to be adjusted moving forward. For instance, my LIRA account was over $40,000 higher than I assumed as I tallied the contributions with 0% growth. It is currently at $171,000 so I need to revise that on my 2017 list.

Below is a list of goals for 2017 that I made in Jan 2016. I have already passed several of these and need to revise up.

OLD GOALS FOR 2017

Have $175,ooo in my self directed investment account*Complete Oct Updated Below*

Have $135,000 in my pension*Complete Updated Below*

Save money for trip to Hawaii with kids

Earn $8,000 yearly in dividend income

Have over $40,000 in cash for market crash*Complete Nov Updated Below*

Increase my margin account to be ready for a market crash.

NEW GOALS FOR 2017

Have $225,000 in personal investment account

Have $175,000 in LIRA pension

Save $50,000 in Cash or HISA or GIC for crash

Increase my margin account to over $50,000

Don’t have a dividend cut

Dividend increases by 50% of my companies

Earn $8,000 in total dividends by the end of 2017

Increase my dividend payout an average of $170 per month ($2,000/12).

Have one month that breaks the $1,000 mark

Have my investments beat the market by over 0.01%

Expectations

I set my goals high.

I’m not sure if I can reach any of these goals let alone all of them, but as long as I’m trying, I’m moving in the right direction. Life has a way of ruining your best laid out plans and I fully expect there to be bumps along the road. The trick is to not get discouraged and keep pushing forward.

As a DGI/Value investor, what are your goals for 2017?

I am not some wunderkind who has a secret you can buy.

I’m not a professional writer, in fact writing is stunningly difficult for me. I even make up fake words that sound real to me on a daily basis. Irregardless, I want to tell my story and help others like me so I push forward.

What I was

I was a below average student that didn’t have much of an interest in scholarly pursuits.

I went to college because I had nothing else to do and after 2 years decided I would take some time off and work. At the time my plan was to work, save money and do some traveling. My dad suggested I get into the trades as I could leave at any time and pick up where I left off.

I applied and quickly started my journey as an apprentice Steamfitter. For those that don’t know (everyone) i’m the guy that puts together any pipe on an industrial level.

At work in Northern Alberta.

Where it led me

Soon after I started my new job (2 months) I met a lovely girl named Kim 🙂 I was renting my friends basement at the time and soon we were living together. After about a year things began to get a little bit cramped. My friend had come home from school in Ontario and we knew something had to change.

At the age of 22 I bought my house.

Not my house 🙂

From the very start I have been frugal. My dad was always perplexed at the fact I didn’t appreciate expensive things. “oh look a Ferrari” -shrug. Even to this day he finds me a bit strange. I work on some of the most expensive yachts in the world, he’s in awe, I think it’s a waste.

At work last week

When I bought my house, I bought what other people would probably consider cheap. Not cheap to me but in a relative Vancouver term.

I would call it affordable.

You see when I bought my house I made sure that I would be able to afford my payments even on unemployment benefits if I lost my job. It was $1300 a month. It sounds cheap now but at the time that was 75% of my wage. Even a cheap house had a lot of risk to me.

I soon started to feel the squeeze of debt. I was able to cover my house payments but there was very little left over after I bought groceries.

Although I was uncomfortable being locked into a mortgage payment I knew there would be some relief. As an apprentice I was guaranteed a raise every 6 months until I finished school and became a journeyman. With this extra money I could take out a loan and pay for a new car or maybe buy a new computer!

How I felt

“Let me tell you why you’re here. You’re here because you know something. What you know you can’t explain, but you feel it. You’ve felt it your entire life, that there’s something wrong with the world. You don’t know what it is, but it’s there, like a splinter in your mind, driving you mad. It is this feeling that has brought you to me. Do you know what I’m talking about?”

Something wasn’t right. I looked around me.

I looked at my friends. Most of them were starting new careers and spending their future earnings based off projected income. Most had new cars, new apartments and new clothes. My friends were going out to parties and movies. They were eating at the best restaurants. They were living good.

I looked at my co-workers. The majority of them were baby-boomers, most were struggling, living paycheck to paycheck. Many could not even afford to retire and were working into their 70’s. “‘How in the world did these poor souls end up in such a bad situation,’ I thought to myself.”

I quickly came to the conclusion that the spending habits of my friend were probably the same as my co-workers when they were young. I didn’t need to read “The millionaire next door” to glean that.

What I did

I hate debt. Let’s just get that out of the way.

One of my favorite quotes in life is “The things you own end up owning you”

Everyone has a different tolerance for debt but I align myself very close to Tyler Durden.

I knew I didn’t want to spend the next 30 years owing the bank interest.

I decided I wanted to do something different.

A change of thinking and expectation was needed as well as a plan.

I decided I didn’t want to work until 70 with a debt load.

I decided to put 100% of my future raises into paying off my mortgage.

This sounds easy but as many people know, life throws in some challenges.

What happened

Everything!

I got married, had our first child and my wife stopped working.

I found out that it was still far too easy to pay all of life’s expenses and double my mortgage payments so I decided to add a couple more kids.

Okay, at this stage I was stretched. I was definitely a house rich, pocket poor guy at this stage. The great part about being poor is that you become a great at DIY projects (okay, maybe just alright).

New roof? I can do that. Breaks on the car? No problem. I learned how to make my own soap, build a staircase, build a backyard deck you name it. I even changed out the bearings on my 07 Honda just to save a few dollars.

PLUS I was starting to see some real progress on my mortgage.

Conclusion

I still have my old mortgage statements where it showed at what date I would be finished my payments.

When I started the end date to be finished was 2032. Every yearly statement that would come in would show a continual progression down in years.

From 2032 to 2027.

The next year would be down again. 2027 to 2024 and so on.

My final payment was June 2013.

I had knocked off 19 years of debt. I was mortgage free before 35. All while living in one of the most expensive cities in North America

The reason this worked out for me is I wanted it. I wanted it more than a new car, more than a trip. I wanted it more than sleep.

When I look around the room at work today and see my co-workers who can’t retire because they need to finish paying off their mortgages, I no longer think how?

Now, I think why?

I never have to worry about a layoff again or how will I feed my children. I will never pay the bank interest just to have a place to live.

I will never let the things I own end up owning me all because I dared to do something different.

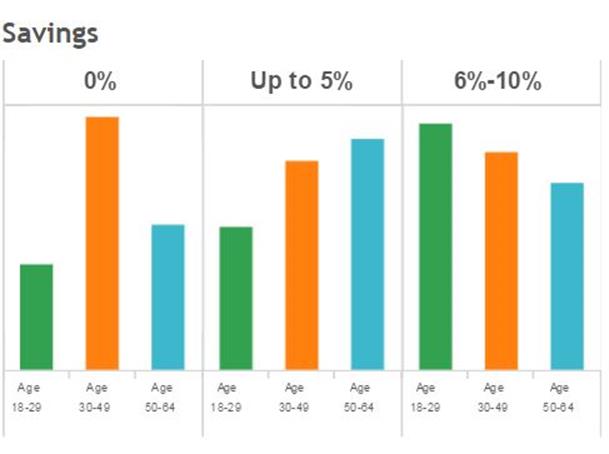

Millennials get a bad rap for not caring about their finances.

But according to a recent Bankrate survey, these young bucks are starting to flip the script and have started saving a bigger chunk of their paychecks than any other age group.

Most millennials are starting to understand the importance of saving money, but it’s tricky to know where to start and what products to trust.

Think investing is only for guys in suits? Nope. This app rounds up every purchase you make to the nearest dolla and invests the difference into a diversified stock portfolio. Once you earn $5, the money can be transferred into your Acorns savings account. Acorns it a great way to start saving automatically with virtually no effort.

This is the first financial app I ever used. I still use it several years later! This money managing app securely connects your financial accounts, automatically organizes and categorizes your expenses, and helps you create a budget. It’s basically shows you your whole financial life and sums it up. Pretty legit.

Digit is a perfect app for someone like myself. Basically it watches your spending and sneaks away a little bit of money every now and again when it (a robot!) thinks you won’t miss it. It sticks the money into a savings account that you can access whenever you want.

Feex is a service that reveals all the fees that you are paying in accounts you invest with. It’s often overlooked, but these fees can be staggering. Feex finds these costs and suggests other options that can bring the fees down. A very handy tool to understand the costs involved

Yes, you need a budget. I don’t use YNAB because I have made my own budget software (and I love spreadsheets) but I know many bloggers who have nothing but praise for this software. YNAB lets you try their budget program for 34 days free so it doesn’t hurt to find out if it’s for you or not. As I mentioned before in my 3 Simple Steps to Becoming Rich, you need a budget one way or another so get on it!

Final Thoughts

Saving money can seem like a daunting task, especially when you have debt to pay back. The trick is to make small automatic contributions that go to a place where it is more difficult to get at and spend. Using these tools will make the path to padding your savings account that much easier.

Disclosure. I’m not getting paid to promote these. Just stuff I personally use.